))

))The aim of this work is to assess the impact mergers and acquisitions have on the value of listed firms in FMCG (Fast Moving Consumer Goods) sector in India. Mergers and acquisitions are a key component of a corporate growth strategy. They are common business tools used worldwide to increase their market share, enhance product offerings and/or diversify the product line, gain access to patents, R&D or technology, attain potential tax benefits, and ultimately maximize shareholder value. These constitute the primary goal of every business firm. The main objective of the present study is to assess the impact of merger and acquisition deals on the financial performance, operating performance, and shareholders' wealth of the sample firms by comparing their performance pre and post the deals. An empirical approach has been taken up to test the hypotheses that were formulated. The present study relies on non-primary sources of data. For all the firms, industry adjusted pre and post-merger/ acquisition ratios have been estimated. Means were also calculated. It is then followed by Paired sample t-test to see if there is any statistically significant difference between the averages pre and post the deals. The overall findings of the study depicted that the financial performance, operating performance, and wealth of the shareholders improved post-merger/acquisition, but the same were found to be statistically insignificant.

Mergers and Acquisitions (M&A) is a worldwide phenomenon. This process of corporate restructuring has a great significance in today's corporate world. Mergers and acquisitions as a part of corporate restructuring strategies are widely being used for growth of an organization and achievement of goals including profit, market monopoly, empire building, and long-term survival. In today's world, companies have to put their best foot forward in order to achieve quality and excellence in their fields.

Every company strives to grow in the most profitable way. The growth for the companies can be plausible both internally and externally. The internal growth of a company can be achieved either by developing new products, sustained improvement in sales, by increasing the capacity of already existing products. External growth is achievable through the strategies of joint ventures, M&As, strategic alliances, takeovers, etc.

However, Mergers and Acquisitions (M&A) are quite popular and important forms of external growth. In our economy which is globalized, mergers and acquisitions are being extensively used for achieving a larger asset base, for penetrating new markets, attaining economies of scope and scale, and attaining complementary competencies and strengths in order to become more competitive than their rivals. The phenomenon of increasing M&A activity is observed across various countries, although, it has commenced much earlier in developed countries (as early as 1895 in US and 1920s in Europe), and is relatively recent in developing countries. In India, M&A activity gained momentum after economic reforms were introduced in the year 1991. Major factors behind the changing trends of mergers and acquisitions in the Indian corporate sector are favorable government policies, additional liquidity in the corporate sector, buoyancy in economy, and dynamic attitudes of the entrepreneurs of India. The increased competition worldwide has in a way coerced the Indian companies to look for mergers and acquisitions as a move of strategic importance.

The trends of mergers and acquisitions in India have undergone drastic changes over the years. The Indian economic reforms since 1991 have thrown ample of challenges both at the domestic level as well as international spheres. In the last two decades, a large number of M&As happen as a strategic choice for attaining sustainable competitive advantage in the corporate world. The policy of liberalization, deregulation and globalization has exposed the corporate sector of our country to domestic and worldwide competition. In recent times, the pace of M&As has increased significantly in India and varied forms of this inorganic growth strategy are visible across different sectors of the Indian economy, viz., finance, oil, pharmaceuticals, telecommunications, computer software, chemicals, and FMCG.

The other sectors in the Indian economy are also following the suit. In a nutshell, mergers and acquisitions (M&As) have evolved as the natural process of business restructuring throughout the world. It has come up as one of the most useful and effective methods of corporate structuring activities and has become an inseparable part of the long-term business strategy of corporate companies across the globe.

Ramakrishnan (2008) has examined whether mergers in India have helped firms perform better in future between the period 1996 to 2002 and has concluded that on an average, merging firms in India performed financially better post-merger, in comparison to pre-merger period. The study also revealed that the long-term post-merger operating profit margin of firms, on an average, improved. Enhanced utilization of their assets by the merging firms resulted in higher operating cash flows. Synergistic benefits appeared to have accrued to the merging entities due to the transformation of the uncompetitive, fragmented nature of Indian firms prior to the merger into consolidated and operationally more viable business units.

Sufian, Muhamad, Bany-Ariffin, Yahya, and Kamarudin (2012) have studied the impact of M&As on the revenue efficiency of banks in Malaysia. The study considered 34 commercial banks during pre-merger/acquisition (1995- 1996) and post-merger/acquisition period (2002-2009). The findings revealed insignificant positive impact on the revenue efficiency of the banks during pre and post-deal periods.

Mahesh and Prasad (2012) have analyzed three Indian Airline companies. The financial performance of these on the post-merger and acquisition, within 2005-2010 period of time were analyzed. Interest coverage, dividend per share, net profit margin, earning per share, and return on equity were the variables used for the study. Besides, paired sample t-test was employed to check for any statistical means difference pre and post the deals. The results show insignificant improvements in the dependant variables undertaken for the study.

Vitale and Laux (2012) have analysed the banking sector in US (post 2007) that included 105 M&As. The results revealed a decline in post-merger/acquisition profitability. There was increase in assets marginally, there was minimal improvement in return and capital adequacy ratios. The study revealed that mergers and acquisitions failed in producing better performing institutions during 2006 to 2008.

Abbas, Hunjra, Saeed, Ul-Hassan, and Ijaz (2014) have examined the performance of banks during pre and post M&As in Pakistan by evaluating 10 banks that have undergone merger or an acquisition during the period, 2006-2011. The results confirmed that there was no significant improvement in the banks' financial performance during post M&A. In addition to this, a decrease in profitability, efficiency, liquidity, and leverage ratios were also reported.

Liargovas and Repousis (2011) have analyzed the impact mergers and acquisitions have on Greek banking sector performance of during the period 1996-2004. This study used samples of 26 Greek commercial banks, where 11 banks were networked in mergers and acquisitions events and 15 banks as non-merger/acquisition. Ratio analysis approach and event study was used to analyze the returns obtained from the stock prices. The overall result revealed there is no positive impact on the operating performance of the banks due to mergers and acquisitions and fail to create significant positive wealth creation for the shareholders as well.

Lai, Ling, Eng, Cheng, and Ting (2015) have analyzed the financial performance of Malaysia local banks during premerger/ acquisition and post-merger/acquisition periods. Paired sample t-test, financial ratio analysis, and data envelopment analysis were used to analyze the leverage, shareholder's wealth, cost reduction profitability, and liquidity as dependent variable. The data was collected from the period 1999-2001 for pre-merger/acquisition and 2002-2010 for the post-merger/acquisition period. The findings of this research indicated no improvement in bank efficiency, productivity level, financial performance, and even cost saving management post-merger or acquisition.

Al-Hroot (2016) have examined the post-merger/ acquisition financial health of seven Jordanian industrial sectors from the period 2000 to 2014. The study analyzed the collected secondary data from various annually published financial statements. Financial ratio analysis and other statistical techniques were used to analyze the significance of pre-post financial performance of selected firms. The results depicted that there was insignificant improvement seen in the post-merger/acquisition period. Market share, liquidity, and profitability showed no improvement in the selected manufacturing firms after the merger and acquisitions deals.

Azhagaiah and Kumar (2011) have assessed the impact of mergers and acquisitions on the financial returns of 12 Indian manufacturing firms from 2004-2010. Accounting ratios, viz., liquid ratio, working capital ratio, and operating ratio were used to study the impact of merger/acquisition three years pre and three years post the deals. Besides, statistical tool parametric t -test was also used to attain the research objectives. The study revealed a significant increase in efficiency, liquidity, profitability, and financial position of the firms post the deals.

Ahmed and Ahmed (2014) have evaluated the impact of merger and acquisitions of manufacturing industries in Pakistan by selecting 12 manufacturing units that have undergone mergers and acquisitions during 2000-09. The study used financial ratios and statistical tools to analyze the significance of pre-post financial performance of selected firms. The results showed that the efficiency of the selected firms deteriorated in post-merger/acquisition period.

Ullah, Farooq, Ullah, and Ahmad (2010) have examined if merger delivers value or not by doing case study of Glaxo Smith/cline merger. They examined the pre and post-merger performance of the firm by using the net present value approach of valuation. The study showed that mega pharmaceutical merger failed to deliver value. The stock prices underperformed both in relative and absolute terms against the index. Instead of a potential employment haven, the merger resulted into substantial reduction in research and development and downsizing.

Kale and Singh (2005) have studied the impact of acquisitions in India in the post liberalization period. The study divided two phases: 1992-1997 and 1998-2002. They noticed a significant difference in the two segments. During the phase of 1992-1997, acquirers in India earned significant positive returns. MNC's acquirer during this phase earned significantly more stock market return in comparison to their local Indian counterparts. There was insignificant difference between related and unrelated acquisitions. Average acquisition returns were much lower during the period_1998-2002 vis-à-vis 1992-1997 periods. The study also concluded that Indian acquisitions have managed to develop their acquisition capabilities over time. During this phase, they found a distinct difference in acquisition value creation between related and unrelated acquisitions. The stock returns were favorable for related acquisitions than for unrelated acquisitions.

Another study that was carried out to determine whether post-acquisition synergy was created leading to improved corporate operating performance and was done by Sharma and Ho (2002). They studied 36 Australian acquisitions which occurred between 1986 and 1991, using matched firms to control for industry and economy-wide factors. Matching was done on the basis of industry and size of assets. Financial ratios pertaining to operating efficiency were used to examine the post-acquisition performance. Operating cash flow before tax was used as the main post-acquisition performance measure. The results depicted insignificant post-acquisition improvement in operating performance. Factors such as relatedness, form of financing, size of the acquisition did not affect postacquisition performance.

Jucunda and Sophia (2014) have analyzed the value creation of bidders in India on acquisition announcement information and the understanding of the stock markets during an announcement. The study used 78 bidder firms in the manufacturing industry who acquired targets in the year 2012. The study showed that acquisitions were not value productive to Indian bidders and those bidders with prior acquisition experience generate more value than single bidder. The results found that acquirers using cash, generate negative returns, and acquirers had a neutral effect on the Indian stock market. The study also found that multiple bidders earned significantly higher abnormal returns than single bidders.

Lau, Proimos, and Wright (2008) have analyzed the operating performance of merging firms, for 72 Australian mergers between 1999 and 2004 and has found improved post-merger operating performance. Industry-adjusted cash flows and efficiency measures were found to be higher in the post-merger period of the sample mergers.

Lowinski, Schiereck, and Thomas (2004) have analyzed the wealth impacts by Swiss corporations of 114 domestic and international acquisitions announced during the period 1990 to 2001. There was no significant difference in wealth creation of acquiring banks between domestic and international acquisitions.

In light of the review of the various studies conducted so far, it was found that some of the studies reported a positive change in performance post-merger/acquisition, while as, some of the studies revealed that the deals were unable to generate positive returns. Thus, it can be inferred that the results by and large were inconclusive.

Merger and acquisition are a firm's set of specific phenomena. However, limited number of studies by far have been conducted to assess the impact of M&As on the individual firms. Such a study would enable to unearth reason for the success or failures of the individual mergers and acquisitions. In the present study, an attempt has been made to explore the impact of mergers and acquisitions on the operating performance, financial performance, and shareowner's wealth of individual sample firms.

The study will also assist investors to make more informed decisions while investing in companies that are about to engage in merger or an acquisition. To the practitioners of management, the study will be helpful in updating themselves and their respective industries on best management practices. The study on M&As not only has significance at the microlevel, but at the macrolevel as well for the economy and the society as a whole. Empirical results about the impact of M&As on the overall performance of the sample merging/acquiring entities would lead to the better policy formulation by the policymakers, thus efficient utilisation of economic resources for the greater economic good of the nation as a whole.

The present study is aimed to achieve the following specific objectives:

In line with the objectives highlighted above, the following hypotheses have been set for the study:

The study has taken into account the secondary data collected from the repository of Centre for Monitoring Indian Economy (CMIE). The financial statements of the selected merging/acquiring firms and merged/target were also collected from the repository of the centre. Besides, many other data sources like sifyfinance, money control, and BSE & NSE publications databases were also used to collect the required data. A case study of five mergers/acquisitions in the FMCG sector have been studied. Financial ratio analysis has been used to compute key financial ratios before and after the merger or acquisition over an eight-year period, four years before the merger or acquisition, and four years post-merger or acquisition. An eight-year gap was quite enough to assess the change in performance. The year of merger/acquisition (year 0), which is the base year has not been taken into consideration because the 0. Figures are affected by onetime merger or acquisition costs borne during that year, making it quite difficult to make the comparison with the results for the other years. Mean differences between pre and post M&A period is important, but more important is to see whether these differences are statistically significant or not. In order to check the statistical significance of mean differences, “two sample paired t-test” was used. The paired two sample t-test is a parametric test used to determine whether the mean difference is statistically significant or not. For the current study, the statistical significance has been checked at 5 percent level of significance.

The financial ratios used to analyse the impact of a merger or acquisition are highlighted as under:

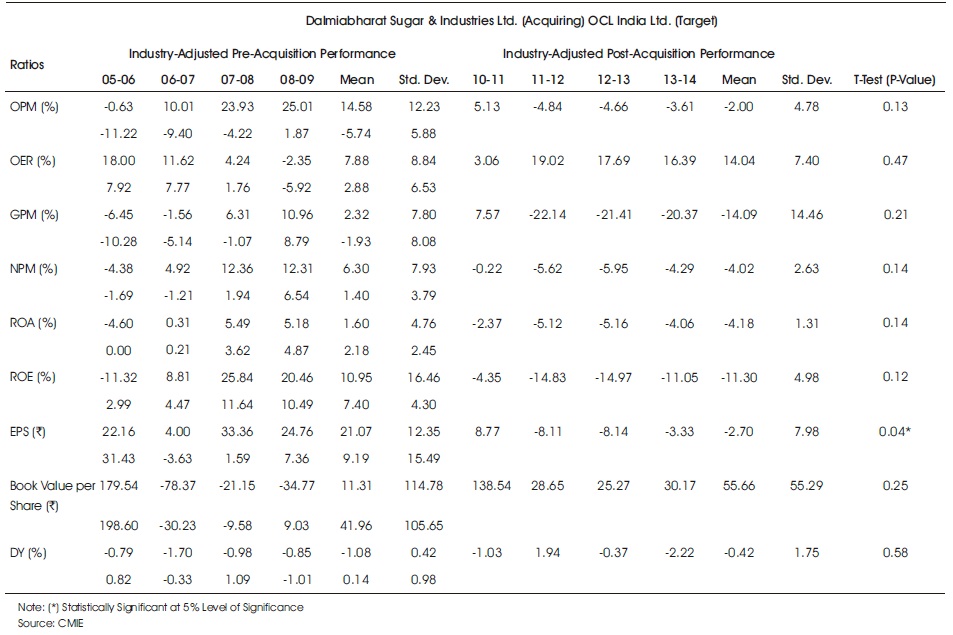

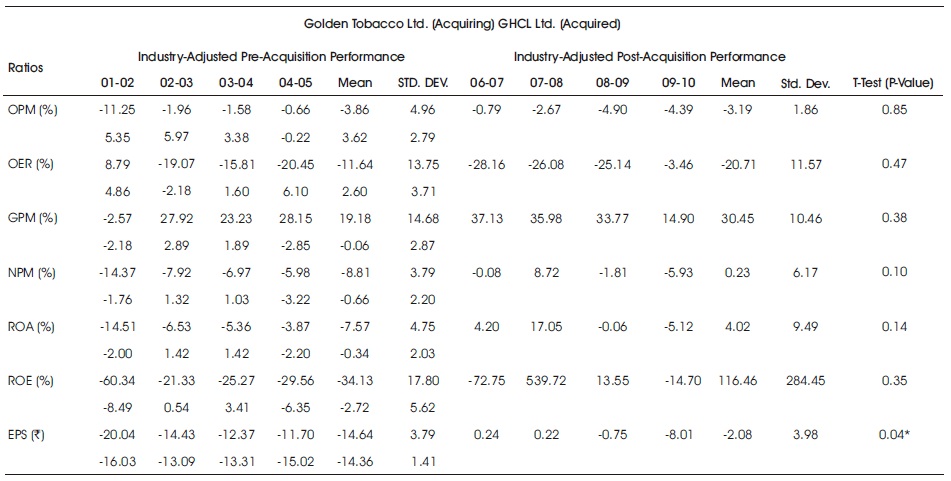

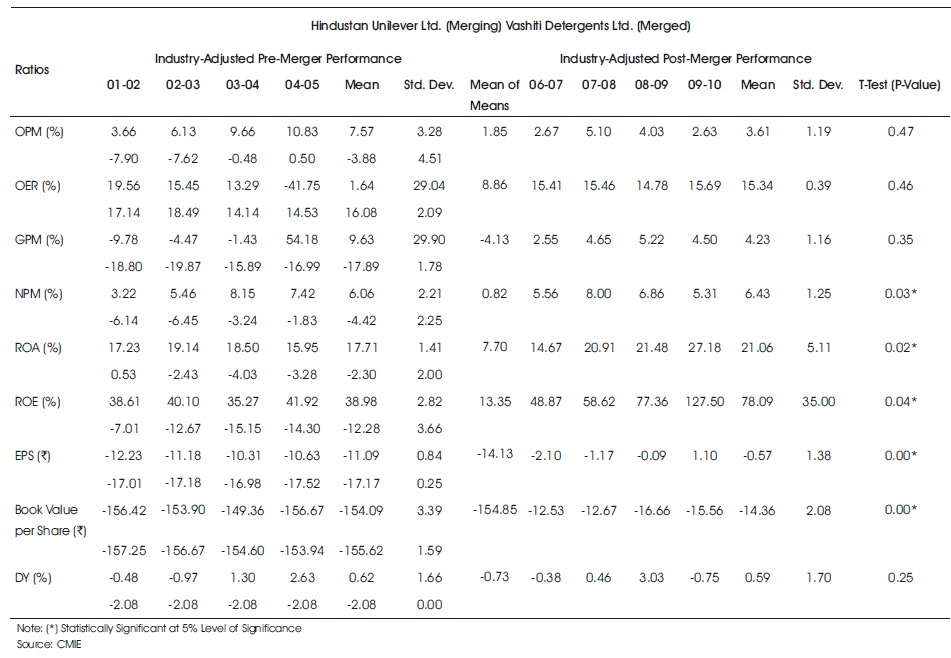

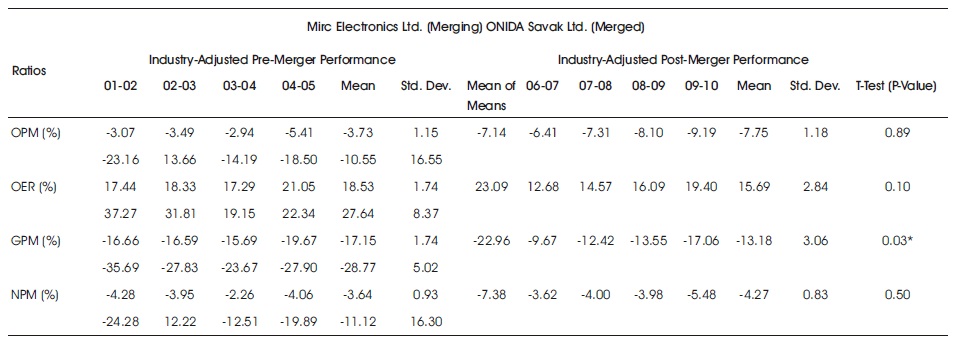

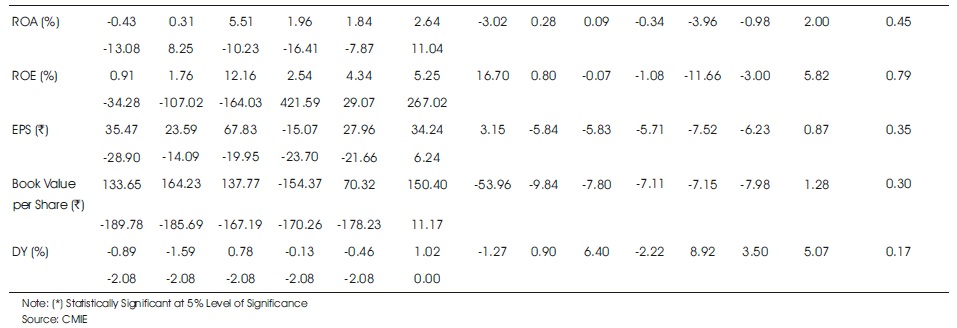

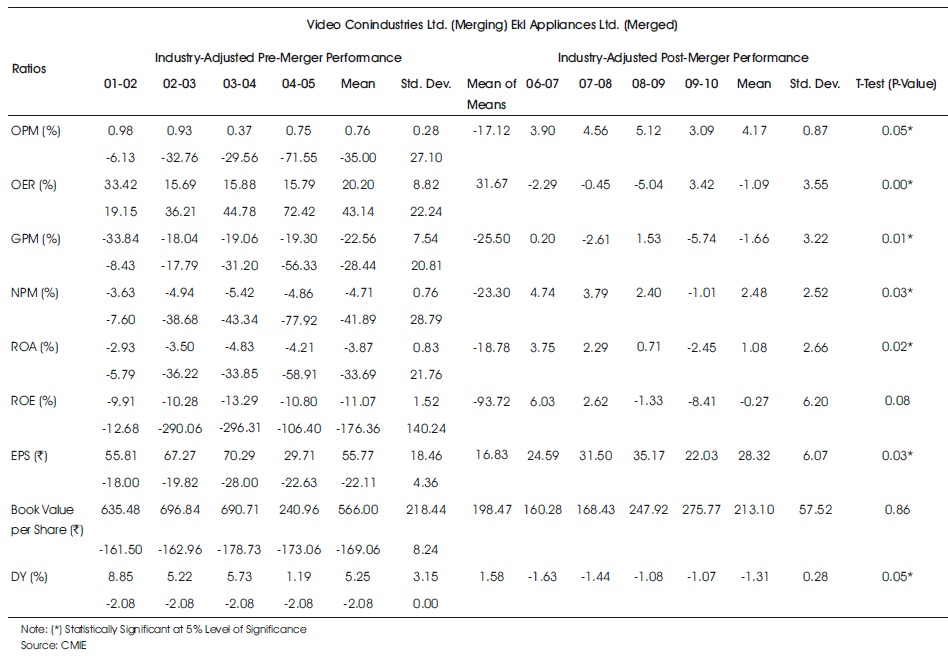

))A sample of five M&As were studied, which included merger of OCL India Ltd. with Dalmia Bharat Sugar & Industries Ltd., acquisition of GHCL Ltd. by Golden Tobacco Ltd., merger of Vashiti Detergents Ltd. with Hindustan Unilever Ltd., merger of Onida Savak Ltd. with Mirc Electronics Ltd. and merger of EKL Appliances Ltd. with Videocon Industries Ltd. (Annexure I). The value of different accounting ratios reflecting financial performance, operating performance, and shareowners wealth of the sample merging/acquiring banks has been presented in Table 1.

Table 1. Different Accounting Ratios-Sample Merging/Acquiring Banks

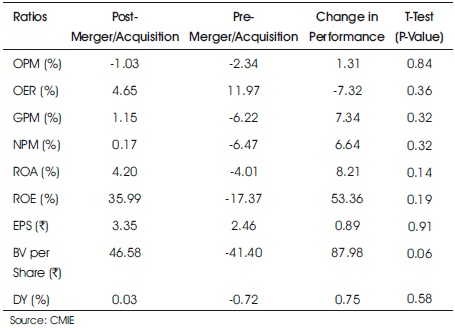

The comparison of the industry-adjusted post and pre mean ratios for the entire sample set of deals revealed that for measures OPM and OER, the M&As have resulted into an improved performance. It is evident from the above table that the industry-adjusted pre-merger/acquisition OPM ratio, which was -2.34 percent has improved to -1.03 percent, thereby, showing an improved operating performance to the extent of 1.31 percent. Similarly, with respect to OER, industry-adjusted OER has declined from 11.97 percent to 4.65 percent post-merger/acquisition reflecting, thereby, improving operating performance to the extent of -7.32 percent. Although, the sample M&As have led to improvements in the industry-adjusted post-merger/ acquisition operating performance of the sample firms, yet their mean difference was not found statistically significant as is evident from the p-values as depicted in the above referred Table 1.

Post and pre industry-adjusted accounting ratios depicting financial performance have also been presented in Table 1. Like for other companies, here also GPM, NPM, ROA, and ROE ratios were used to assess the financial performance of the sample merging and acquiring firms. Perusal of these ratios have shown that the sample firms have seen improvements in their financial performance post-merger or acquisition. It is evident from the above table that all these four ratios have recorded improvements post M&A. The industry-adjusted pre M&A mean value of GPM, NPM, ROA, and ROE, which was -6.22 percent, -6.47 percent, - 4.01 percent and -17.37 percent has increased to 1.15 percent, 0.17 percent, 4.20 percent, and 35.99 percent, respectively, thereby reflecting an improvement in the overall profitability of the sample firms. The mean difference in performance for all the ratios is not found statistically significant as is evident from their p-values.

From the data given in Table1, it becomes clear that the sample firms have recorded an increase in shareowners' wealth post M&A. This is evident from the positive mean differences of EPS, BV & DY variables. It is evident from the table that the EPS, BV & DY has increased by 0.89, 87.98, and 0.75%, respectively. However, the mean difference between industry-adjusted pre & post M&A values for all the ratios has been found statistically insignificant at 5 percent level of significance as becomes clear from their p-values.

The decisions for M&A may have been inspired by other motives like overpayment, empire building, integration issues, etc., which eventually causes profits to suffer leading to wealth destruction for shareholders as well. To justify their actions, Merger and acquisition makers often cite synergy as the main motive behind such deals (Porter, 1989). The objectives of the M&As are attaining financial synergies in terms of lowering the cost of capital, operational synergies in terms of offering unique products and services and managerial synergies through superior planning and monitoring qualities of the managers (Seth, Song, & Pettit, 2000). But they have been criticized as concepts are often talked about but seldom realized (Kitching, 1967; Porter, 1989). As per the valuation approach, mergers and acquisitions are planned and executed by managers who believe in the theory that they have unique information about the target's value than the stock market and hence the plausible advantages to be derived from combining the target's businesses with their own (Holderness & Sheehan, 1985). This is one of the major causes behind majority of the deals not performing up to the mark. Expectation of higher profitability dwells from overpayment. Excessive goodwill as a result of overpaying needs to be written off, which leads to a decline in the profitability of the firm. The hubris hypotheses states that the announcement of an acquisition does not lead to return for the acquiring firm, but leads to transfer of the wealth from the biding shareholders to the target shareholders (Jensen, 1984). Managers fail sometimes to select the right target. Another rationale behind the failure of M&A to generate the real benefits could be attributed to empire-building theory. Managers who maximize their own wealth at the expense of the shareholder plan and execute Mergers and acquisitions. Managers' salaries, bonuses, promotions, prestige, and power are all related to the change in size and growth of the company rather than to its profitability (Mueller, 1969). Many integration problems have been seen to occur when firms merge or get acquired. The differences in managerial styles, lack of planning, work ethics, control systems, threat of layoffs, the compensation inequalities, and more may bring about inefficiencies that nullify the possible benefits of merger (Leibenstein, 1966). Besides these, cultural differences have assumed great importance. Culture differences act as a key element affecting effectiveness of the integration process and consequently the success of M&As. They need to be flexible and adaptable. Inadequate understanding of such cultural differences has led to the failure of several M&A deals to deliver the desired results (Rottig, 2007). Besides these, economic disturbances and political influences (Gort, 1969) are also found to be the reasons for mergers and acquisitions leading to uncertainty in the outcomes.

The findings of the study have indicated that there are finally growth in assets, reduction in expenses, increase in profitability margins, and returns to the shareholders. However, all the changes in performance is found statistically insignificant for all the ratios. From above analysis, it may be concluded that the financial performance, operating performance, and shareholders' wealth for the sample firms in this industry has improved post-merger or acquisition, but no improvements were found statistically significant. The firms have not been quite effective and efficient to use this route of corporate restructuring to consolidate their business operations and enhance their competitiveness in the market. The probable reasons for such results could be that such decisions are not fully focused at maximizing the company's profits and henceforth, the wealth of shareholders. Most of the researchers agree that mergers and acquisitions are driven by a complex pattern of motives, and there is no single approach that can render a full account. However, it is important for firms to generate elevated profits after the mergers and acquisitions in order to rationalize the decision behind such deals.

Keeping in consideration the probable reasons that have been put forth above and the findings of the present study, following suggestions by the researcher are being offered.

Mergers and acquisitions have plethora of opportunities for future research and hence there is consensus on its exploration. In order to obtain greater insight on the subject, various recommendations for further investigation are provided.

The results of any study should be considered with a degree of knowledge of its limitations. The following limitations of the study have been put forth.